CalSTRS Exaggerates Costs of Divestment

CalPERS and CalSTRS manage portfolios worth $466 billion and $323 billion, respectively, so it’s natural for these public pension funds to throw around large numbers. But evidence from the funds themselves and from independent analyses suggests that PERS and STRS wildly exaggerate both the transaction costs and the opportunity costs of divestments in general.

In two recent hearings on the fossil fuel divestment bill SB 1173, CalSTRS’ governmental affairs director Joycelyn Martinez-Wade confidently asserted that CalSTRS’ past divestment actions have cost the fund “$9 billion dollars.”

And in the California Senate Informational Hearing on Pension Funds on March 9, 2022, CalSTRS CIO Chris Ailman asserted that “every divestment has cost us money.” He added that the “thermal coal divestment has come the closest to breaking even,” but still represented a loss for the portfolio.

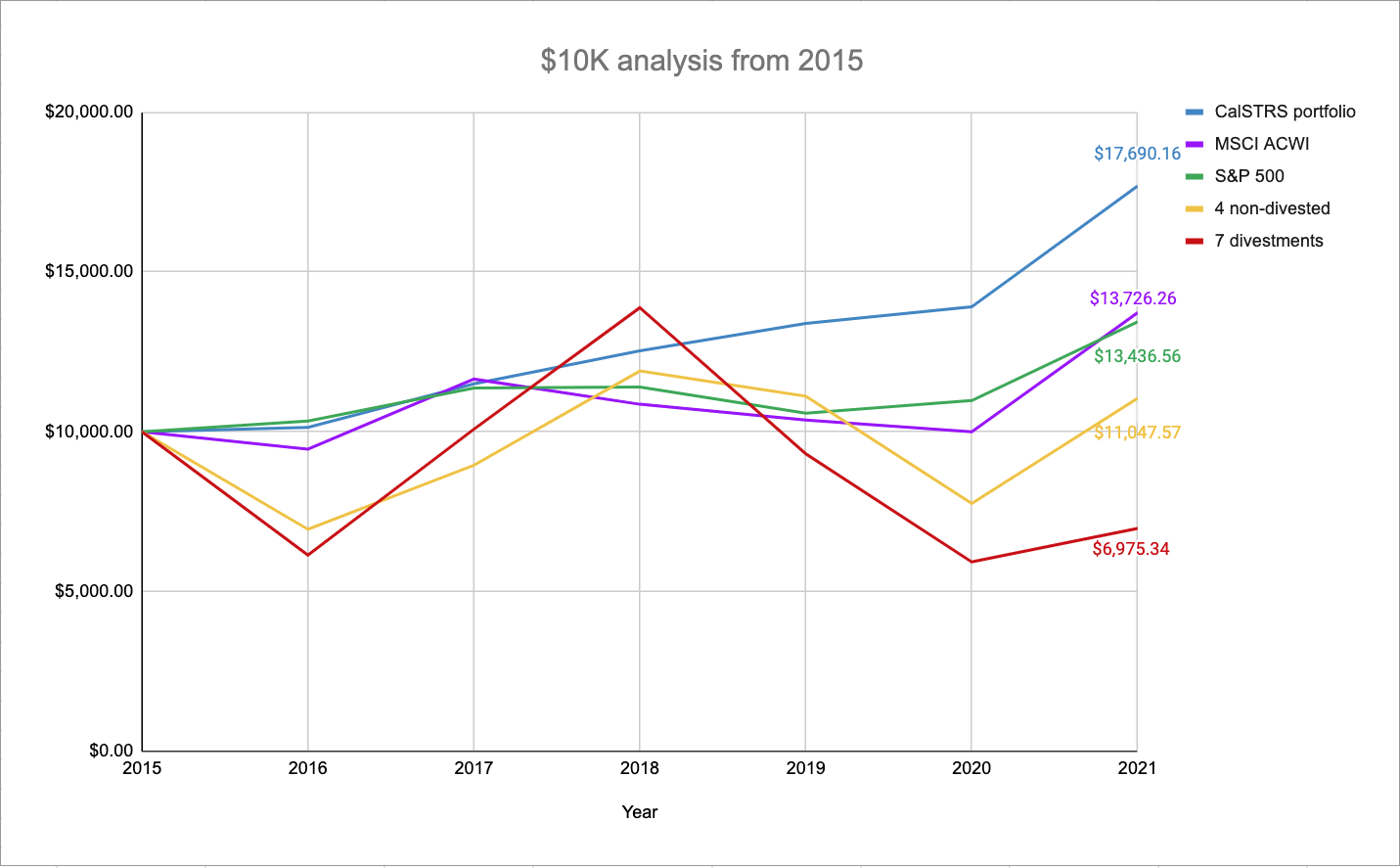

To test this assertion about the impact of divesting from thermal coal, UC Berkeley Economics students Lanie Goldberg and Owen Doyle charted the value of a $10,000 investment over the years 2015-2021 for the seven thermal coal companies that CalSTRS divested [mandated by SB185 to be completed by 2017], and compared the performance to standard benchmarks and the CalSTRS portfolio as a whole.

Their finding: The divested thermal coal companies lost money, so divestment improved the CalSTRS portfolio earnings. An initial $10,000 investment in the 7 thermal coal companies that CalSTRS divested would be worth about $6,975 in 2021. That means that by divesting its $9.8 million investment, CalSTRS avoided losing $3 million.

The above chart estimates the returns on an investment of $10,000 from 2015-21 (as of June 30 close for each year) under various scenarios. Performance of the 7 divested thermal coal companies (red) is plotted along with the CalSTRS portfolio (blue), and standard benchmarks S&P 500 (green) and the MSCI ACWI (purple).

Findings

- An initial $10,000 investment in the 7 thermal coal companies that CalSTRS divested would be worth about $6,975 in 2021. That means that by divesting its $9.8 million investment, CalSTRS avoided losing $3 million.

- CalSTRS still holds 4 thermal coal companies: BHP Billiton, Glencore, PTT PLC, and Sasol. (Divestment of these companies was not required under the terms of the SB 185 legislation.) The investment in these companies (yellow) did a little better than break-even ($11,047), but they did not perform as well as standard benchmarks or the overall CalSTRS portfolio. There was no compelling reason to stay invested.

- At $17,691, CalSTRS portfolio performance outperformed standard benchmarks, reaching record profitability despite the assertions about the effect of divestments. As shown, the overall portfolio vastly outperformed the money-losing coal companies.

Background Reference: What Was Divested?

- U.S. Thermal Coal (May 2016): CalSTRS sold an estimated $1.5 million from affected holdings in CalSTRS’ U.S. Equity and Fixed Income Portfolios, as of December 31, 2015. The affected companies are: Cloud Peak Energy; Hallador Energy Company; Peabody Energy Corporation; and Westmoreland Coal Company.

- Non-U.S. Thermal Coal (June 2017): CalSTRS sold approximately $8.3 million in three companies: PT Adaro Energy, based in Indonesia; Exxaro Resources Limited of South Africa; and the Australian company, Whitehaven Coal Limited.

Table 1: Share Price History of Divested Companies (closing share price on June 30th of the given year). The “0” values represent bankruptcy or a pause in trading (Peabody).

* Cloud Peak Energy declared bankruptcy in 2019. Westmoreland declared bankruptcy in 2018 and reorganized as a private company.

** Peabody Energy declared bankruptcy in 2016; it reorganized in 2017, but shares were not available to institutional investors.

Like other fossil fuel investments, thermal coal investments are risky and volatile. Staying invested in fossil fuels has cost both CalSTRS and CalPERS billions in lost value over the years. For example, Peabody Coal (divested by both Funds in response to SB 185) had already lost most of its value by the time it was divested. And, even with surging coal share prices, Peabody Coal is still not a good investment. Despite recent price spikes, Peabody (bankrupt 2016; reorganized 2017; fluctuating wildly ever since) has returned -3.54% over the past 5 years, according to Yahoo! Finance charts.

The CalSTRS report on its thermal coal divestments also cites the decline in value of the thermal coal investments as a reason why the thermal coal divestments had no significant impact on the portfolio. To quote the report: “At its February 3, 2016, meeting the board voted to divest of U.S. thermal coal companies as they had become de minimis to the portfolio….At its June 7, 2017, meeting, the board voted to divest of non-U.S. thermal coal companies as they had become de minimis to the portfolio.”

By its own admission and confirmed by the UC Berkeley analysis, there’s no way that divestment of seven (7) thermal coal companies cost CalSTRS money. In fact, restricting these investments prevented CalSTRS from losing millions. The real question is, “Why didn’t CalSTRS divest sooner?”